The purpose of a proration in a sale transaction is to fairly divide property expenses like taxes and association dues between the Seller and Buyer so that each party is paying only for those days which he actually owns the property.

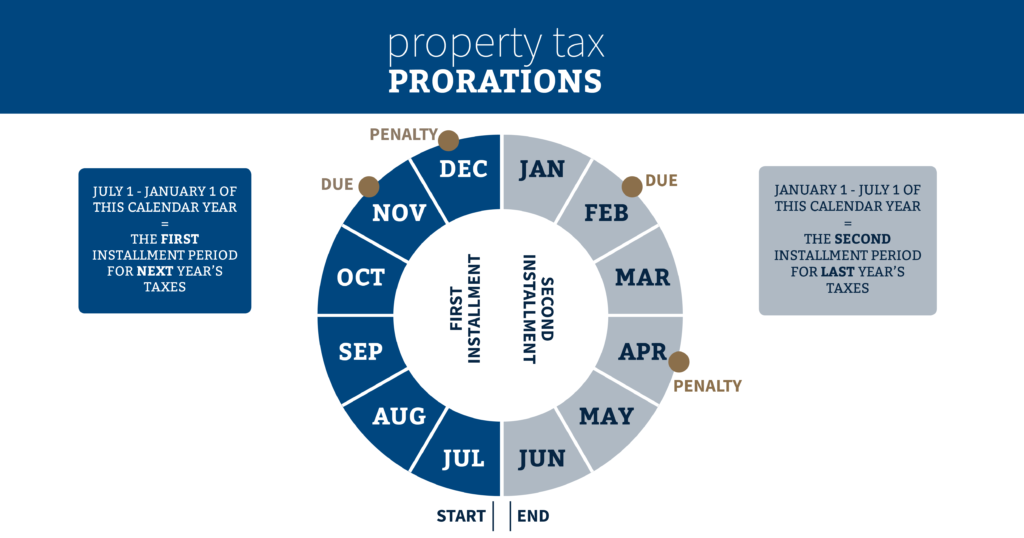

The property tax year does not follow the standard calendar year. The tax year runs from July 1st of one calendar year to July 1st of the next. For example, a tax year might be described as the 2018-2019 tax year, meaning the time period from July 1, 2018 to July 1, 2019.

The tax year is divided into two installments..

The 1st installment period runs from July 1st to January 1st. The payment for this period is due on November 1st and is delinquent and subject to penalty after December 10th.

The 2nd installment period runs from January 1st to July 1st. The payment for this period is due on February 1st and delinquent and subject to penalty after April 10th.

Determine the date to which taxes are paid:

- If the Seller (or escrow holder) pays (or has paid) the 1st half, then taxes are paid to January 1st

- If the Seller (or escrow holder) pays (or has paid) the 2nd half, then taxes are paid to July 1st

If the Seller’s last tax payment covered an installment period which extends beyond the close of escrow, the proration is made from the close of escrow to the date to which the taxes are paid. The proration is a credit to the Seller and a charge to the Buyer.

EXAMPLE

Close of escrow is November 22, 2018. Seller pays the 1st installment of taxes which brings the taxes current to January 1, 2019. Seller is credited and Buyer is debited from November 22, 2018 to January 1, 2019. This reimburses the Seller for the days within that tax period that he no longer owns the property.

If the escrow closes before the tax due date arrives for a particular tax period, the proration is made from the first day of the installment period to the close of escrow. The proration is a charge to the Seller and a credit to the Buyer.

EXAMPLE

Close of escrow is January 15, 2019. Seller has NOT paid (and is not required to pay) the 2nd installment. The payment for this installment will become due when the Buyer is the owner of the property (after the close of escrow). Seller is debited and Buyer is credited from January 1, 2019 to January 15, 2019. The Buyer is responsible for payment of the 2nd installment which is due February 1st, and this proration offsets the Buyer for the days that the Seller owned the property within the covered tax period. (If the Buyer is obtaining new financing, the lender is likely to require that the Buyer pay this tax bill through escrow because the due date is imminent).

At closing, if the Seller has not yet made a payment which is due, the Seller is charged through escrow with the amount of the installment. If a lender in a transaction requires that a future tax payment be made, this payment is a charge to the account of the Buyer. The Seller is only responsible for making tax payments that come due during the time period that the Seller owns the property.

The Buyer becomes the owner of the property on the day of closing (is considered the owner for the full day on which the Grant Deed in his favor is recorded in the public record, regardless of the hour of the recording), so the Buyer is responsible for the tax bills that come due on or after that date.